A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution

– Satoshi Nakamoto, Bitcoin Whitepaper

Every time you make an online purchase, your payment travels through a complex web of financial intermediaries – each adding time, cost, and complexity to a seemingly simple transaction. While this system works, it’s built on decades-old infrastructure that was never designed for the digital age. Blockchain technology offers a fundamentally different approach to moving money.

The Traditional Payment System

To understand how blockchain transforms online payments, let’s first break down who is involved and what actually happens between clicking ‘pay now’ and receiving your order confirmation.

Key Players in Traditional Payments:

- Issuing Bank: Customer’s bank that issues payment cards and authorizes transactions

- Card Networks: Connect banks and processors, set system rules ie. Visa, Mastercard

- Payment Processor: Handles technical infrastructure for card payments ie. Stripe, Square

- Acquiring Bank: Partners with processors to settle funds and manage risk

- Settlement Networks: Move money between banks after approval

Step-by-Step Payment Journey

- Transaction Initiation

- You enter card details or select saved payment method

- Merchant’s payment gateway encrypts and sends data to payment processor

- Authorization Request

- Payment processor, via acquiring bank, sends request to card network

- Card network forwards to your bank (issuing bank) for verification

- Your bank checks funds, card validity, and fraud indicators

- Authorization Response

- Issuing bank reserves the funds and sends approval code

- Response flows back through card network to processor

- Processor confirms approval to merchant

- You see “Payment Successful” message

- Settlement Process

- At end of business day, merchant submits batch of approved transactions

- Payment processor consolidates and routes to card networks

- Card networks sort transactions by issuing bank

- Banks exchange funds through settlement networks

- Final Settlement

- Acquiring bank credits Merchant’s account (minus fees)

- Your bank posts transaction from “pending” to “posted”

- Process takes 2-3 business days

Payment Fees

The typical online payment fee *starts at 2.9% + $0.30 and is roughly split as follows:

- Interchange Fee: **1.0-2.0% (to issuing bank)

- Network Fee: 0.14% + $0.10 (to card networks ie. Visa)

- Processing Fee: 0.5-1.5% (to processor/acquiring bank)

*This base rate can increase further when processing international cards, handling currency conversions, or utilizing additional services offered by the payment processor. International cards and currency conversion alone can nearly double the payment fee. See Stripe Pricing.

**Interchange fee is set by card networks and varies based on product category and card type. See Visa’s latest Interchange rates.

You can see how this fee structure particularly impacts smaller purchases. For example:

- On a $4 coffee: $0.42 (10.5% of sale)

- On a $10 purchase: $0.59 (5.9% of sale)

- On a $100 purchase: $3.20 (3.2% of sale)

Consider a coffee shop making $2 net profit per cup, these payment fees consume about 20% of their profit margin! This impact is more severe for small independent businesses with tighter margins, especially since they lack the sales volume needed to negotiate lower processing rates.

Beyond the base processing fees, merchants also face risks from chargebacks – where customers can dispute and reverse charges up to several months after purchase. Each chargeback typically incurs an additional fee of $20-100, regardless of whether the merchant wins the dispute. Frequent chargebacks can also lead to higher processing fees or even account termination.

The reversible nature of traditional payments creates additional operational overhead for merchants who must maintain dispute management processes and reserve funds to cover potential chargebacks.

Key Points

- Settlement takes 2-3 business days as transactions move through multiple verification and batch processing steps

- Standard payment fees start at 2.9% + $0.30 per transaction, with fees increasing significantly for international cards, currency conversion, and additional processor services

- Payment fees make microtransactions impractical and more heavily impact small businesses as they can’t negotiate better processing rates

- The current infrastructure was not designed for the digital age, adding unnecessary time, cost, and complexity to online transactions

- The reversible nature of payments through chargebacks creates additional costs and operational complexity for merchants, who face fees of $20-100 per dispute

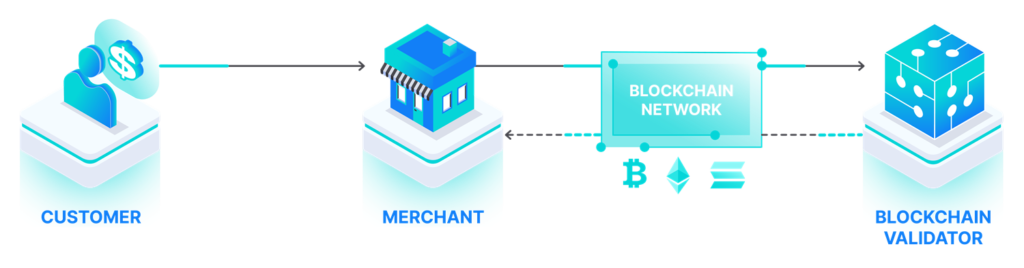

The Blockchain Payment System

Blockchain technology reimagines this entire process by replacing intermediary trust with cryptographic verification. Instead of banks and processors validating transactions, a network of independent validators works together to verify and record each payment.

Key Players in Blockchain Payments:

- Network Validators: Independent operators who run nodes that verify transactions and maintain copies of the blockchain. They replace the role of banks and processors in verification.

- Network Protocol: The software rules that govern how transactions are processed and verified. This replaces the role of card networks in standardizing communications.

- Wallet Software: Applications that help users manage their private keys and create transactions. This replaces the role of banks in storing and managing funds.

Blockchain Payment Journey

- Transaction Creation

- Enter payment details and authorize with your private key

- Similar to entering card details, but more secure

- Wallet adds network fee paid to validators

- Network Broadcasting

- Transaction sent directly to network validators

- No banks or processors needed to route payment

- Verification Process

- Validators check your balance and signature

- Multiple validators verify at once, unlike banks’ sequential approvals

- Settlement

- Payment recorded on blockchain

- Funds available instantly to recipient

- No multi-day waiting period

Note: Details vary between blockchains (Bitcoin, Ethereum, Solana etc.), but they all share this core process of replacing intermediaries with network verification.

Fee Comparison

The following are based on a simple transfer action.

| Transaction Amount | Traditional (Stripe) | Bitcoin | Ethereum | Solana | Base |

|---|---|---|---|---|---|

| $1 | $0.33 (33%) | $1.00-4.00 | $1.00-5.00 | <$0.01 | <$0.01 |

| $10 | $0.59 (5.9%) | $1.00-4.00 | $1.00-5.00 | <$0.01 | <$0.01 |

| $100 | $3.20 (3.2%) | $1.00-4.00 | $1.00-5.00 | <$0.01 | <$0.01 |

| $10,000 | $290.30 (2.9%) | $1.00-4.00 | $1.00-5.00 | <$0.01 | <$0.01 |

Bitcoin and Ethereum fees are heavily impacted by transaction activity on their respected chains. That of course isn’t ideal for consumer payments, but you have many low fee options like Solana or Ethereum L2’s such as Base and Optimism.

The pros and cons of each chain I’ll get into in a future post, for now just know that consumer focused blockchains have near $0 fees and economically make more sense for payments, especially microtransactions.

Key Points

- Simpler and Faster: One system handles the entire payment, settling in minutes instead of days through multiple companies

- Lower Costs: Single small network fee replaces multiple percentage-based fees from banks, processors, and card networks

- Truly Global: Same process and cost whether sending across town or across the world, working 24/7 without banking hours

- More Control: Track your transaction at every step and access funds immediately, with no third party able to block or delay access

- Better Security: Mathematical verification and permanent record-keeping replace trust in multiple financial institutions

The Road to Adoption

For cryptocurrency payments to become mainstream, two critical pieces need to align: business infrastructure and user adoption. Both are evolving faster than many realize.

Payment Processor & Merchant Integration

Payment processors like Stripe (who recently acquired a major *stablecoin platform for $1.1 billion) are already integrating crypto payments because it offers clear advantages:

- Better Economics: Processors can offer lower fees by bypassing card networks and bank fees, creating a win-win where both processors and merchants save money

- Easy Integration: Merchants can accept crypto through their existing payment processor relationships with minimal system changes

- Faster Settlement: Merchants can access funds within minutes instead of waiting days for traditional bank settlement

- Customer Incentives: Merchants can share their fee savings with customers through rewards or discounts when crypto payments are used

Visa recently announced VTAP (Visa Tokenized Asset Platform), using the Ethereum network to enable banks to bring fiat currencies onchain in a safe, seamless, and efficient manner. One of the key benefits they mention is near real-time settlement onchain.

*Stablecoins are cryptocurrencies designed to maintain a constant value of $1 by being backed by a combination of US dollars and short-term US government obligations held in reserve. They function as a digital version of the US dollar on the blockchain, allowing for faster and easier transactions in the crypto ecosystem while providing stability through their backing of highly liquid, regulated assets.

User Adoption

The key to widespread crypto payments is users having digital wallets, which is already happening through various entry points:

- Trading & Speculation: Many create wallets for cryptocurrency trading or investing, and while often viewed controversially, this has significantly driven wallet adoption and familiarity with crypto payments

- Financial Access: In countries with weak banking infrastructure or high inflation, crypto provides essential financial services and a stable store of value

- International Remittance: Migrant workers use crypto to send money home, avoiding high fees and delays of traditional money transfer services

- Digital Assets: Artists, collectors, and gamers create wallets to buy, sell, and trade digital art, collectibles, and in-game items

- DeFi: Users access financial services like lending, borrowing, and earning yield through decentralized protocols that operate without traditional banks

Once users have a wallet – regardless of why they created it – they’re equipped to use crypto payments whenever beneficial, especially if merchants were to offer incentives.

This evolution is already underway. As payment processors integrate blockchain settlement and more users gain access to digital wallets, we’ll see a gradual shift toward more efficient payment infrastructure – without requiring massive changes to how we shop online.